Free Economic Zones

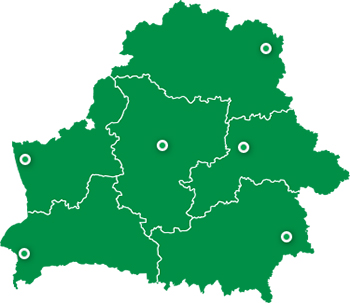

Six free economic zones were established in the Republic of Belarus: FEZ Brest (1996), FEZ Vitebsk (1999), FEZ Gomel-Raton (1998), FEZ Grodnoinvest (2002), FEZ Minsk (1998) and FEZ Mogilev (2002). They provide their residents with more favorable than generally established conditions for the implementation of investment and business activities.

Six free economic zones were established in the Republic of Belarus: FEZ Brest (1996), FEZ Vitebsk (1999), FEZ Gomel-Raton (1998), FEZ Grodnoinvest (2002), FEZ Minsk (1998) and FEZ Mogilev (2002). They provide their residents with more favorable than generally established conditions for the implementation of investment and business activities.

Free economic zones were created to attract investments in the creation and development of export-oriented and import-substituting industries based on new and high technologies. Hence, the framework of a special tax regime was determined, which applies to the sale of goods (works, services) by residents of the free economic zones of their own production:

- outside the Republic of Belarus to foreign legal entities and (or) individuals;

- on the territory of the Republic of Belarus to other residents of the free economic zone;

- on the territory of the Republic of Belarus, if the goods (works, services) are import-substituting in accordance with the List determined by the Government of Belarus.

Tax benefits for project in the free economic zone:

Exemption from:

Corporate Income Tax (1)

Real Estate Tax (2)

Ground Rent (3)

Land VAlue TAx (4)

Custom Duties (5)

Work and residence permit fees (6)

Compenstion of forestry and agricultural production losses

Comments:

(1) — Exemption from export sales and to other FEZ residents;

(2) — Exemption from taxation on the territory of FEZ within three years from the date of registration; Exemption from export sales and to other FEZ residents. The exemption applies to profits from the sale of goods (works, services) of own production.

(3) — Exemption for the period of design and construction of facilities, but not more than five years from the date of registration. Exemption regardless of the direction of their use (for export and (or) to other FEZ residents);

(4) — Exemption for the period of design and construction of facilities, but not more than five years from the date of registration. Exemption regardless of the direction of their use (for export and (or) to other FEZ residents);

(5) — Exemption from import customs duties, taxes in respect of goods placed under the customs procedure of the free customs zone. Exemption from VAT levied by customs authorities on goods placed by FEZ residents under the customs procedure of release for domestic consumption, manufactured with the use of foreign goods placed under the customs procedure of the FEZ;

(6) — Exemption for issuance of special permits for employment in the Republic of Belarus.

Other benefits:

♦ Exemption from payment for the right to conclude a land lease agreement.

♦ Financing of expenses for the creation of engineering and transport infrastructure at the expense of funds provided in the State investment program and local budgets, in the case the FEZ resident's implements the investment project with the declared investment volume of more than 10 million Euros